Calendar events: FOMC / CPI / NFP reactions

DoneCalendar events: FOMC / CPI / NFP reactions

2026-05-17 · status: done · 1.0s

Hypothesis: BTC reacts directionally to US macro releases (FOMC, CPI, NFP). For at least one event type and one horizon, the post-release mean forward return exceeds 30 bps with |t-stat| > 2 vs same-hour non-event baseline.

Verdict: FOUND DIRECTIONAL EDGE — FOMC releases predict +50.0 bps fwd-1h returns (t = +2.28, n_event = 52) vs same-hour baseline. Worth building a calendar-gated entry around this.

Key metrics

| metric | value |

|---|---|

| events_tested | ['FOMC', 'CPI', 'NFP'] |

| n_passes | 1 |

| strongest_event | FOMC |

| strongest_horizon | 4h |

| strongest_diff_bps | +67.0755 |

| strongest_t_stat | +1.8691 |

| best_vol_lift_x | +2.8925 |

| best_vol_lift_event | FOMC |

Approach

Hardcoded FOMC meeting dates 2020-2026 (statement at 14:00 ET). CPI and NFP timestamps generated from the standard release rules (second Tuesday / first Friday of each month at 8:30 ET). DST handled. For each event we take the closest hourly close as the anchor and compute log return over 1h / 4h / 1d horizons after.

Baseline: forward returns at non-event hours matching the same hour-of-day as the event type, excluding ±24h windows around any event.

Promote gate (directional): one event × horizon with |mean fwd| > 30 bps, |t-stat vs baseline| > 2.0, n ≥ 30.

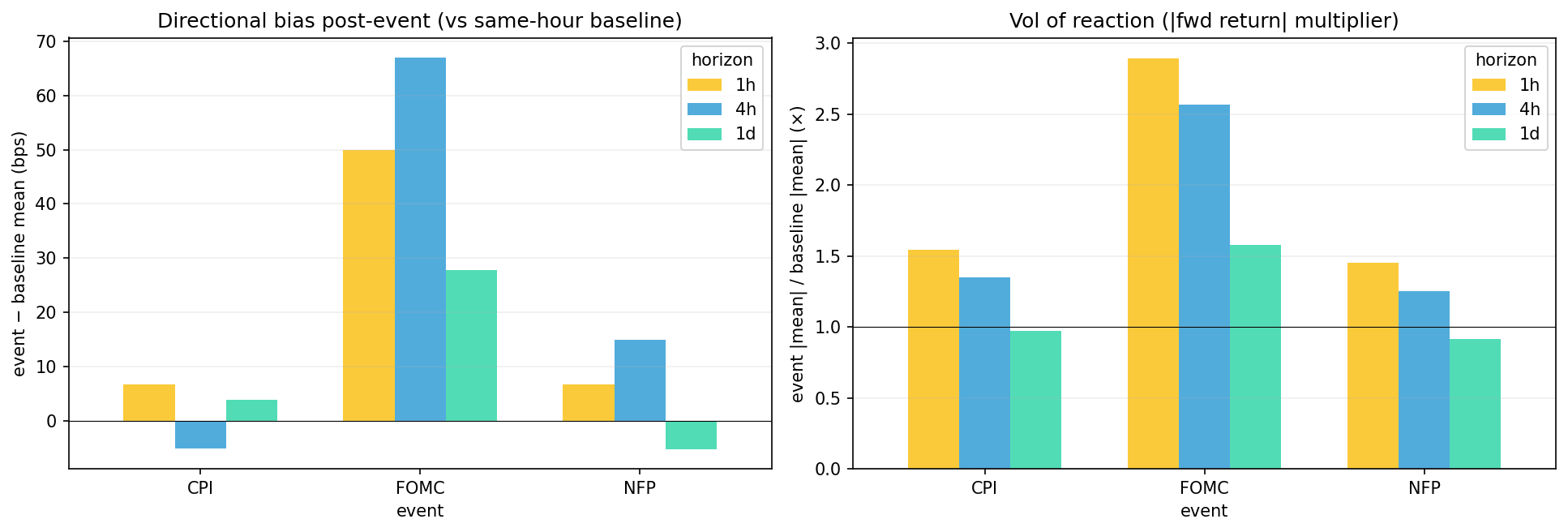

1. Directional reaction (signed return)

diff_bps = event mean − baseline mean (signed). t_stat_vs_baseline is the Welch t-statistic. |t| > 2 + |diff| > 30 bps = passable.

| event | horizon | n_event | event_mean_bps | baseline_mean_bps | diff_bps | t_stat_vs_baseline |

|---|---|---|---|---|---|---|

| FOMC | 1h | 52 | 49.9 | -0.12 | 50 | 2.28 |

| FOMC | 4h | 52 | 73.8 | 6.76 | 67.1 | 1.87 |

| FOMC | 1d | 52 | 37.1 | 9.3 | 27.8 | 0.42 |

| CPI | 1h | 77 | 8.1 | 1.45 | 6.7 | 0.47 |

| CPI | 4h | 77 | -3.7 | 1.5 | -5.2 | -0.24 |

| CPI | 1d | 77 | 12.8 | 9 | 3.8 | 0.11 |

| NFP | 1h | 77 | 7.9 | 1.28 | 6.6 | 0.68 |

| NFP | 4h | 77 | 17.4 | 2.5 | 14.9 | 0.74 |

| NFP | 1d | 77 | 6.2 | 11.48 | -5.3 | -0.14 |

2. Vol-of-reaction (mean |fwd return|)

Even if direction is random, events typically cause larger post-event moves than non-event hours. abs_lift_x shows the multiplier (>1 = event hours have bigger moves on average).

| event | horizon | event_abs_mean_bps | baseline_abs_mean_bps | abs_lift_x |

|---|---|---|---|---|

| FOMC | 1h | 115.4 | 39.9 | 2.89 |

| FOMC | 4h | 197.9 | 77.1 | 2.57 |

| FOMC | 1d | 332.6 | 210.9 | 1.58 |

| CPI | 1h | 67 | 43.5 | 1.54 |

| CPI | 4h | 136.7 | 101.3 | 1.35 |

| CPI | 1d | 203.9 | 210.2 | 0.97 |

| NFP | 1h | 64.9 | 44.7 | 1.45 |

| NFP | 4h | 129.6 | 103.7 | 1.25 |

| NFP | 1d | 196.9 | 215.6 | 0.91 |