FOMC Stage-2: stress-test the +50 bps fwd-1h drift

DoneFOMC Stage-2: stress-test the +50 bps fwd-1h drift

2026-05-17 · status: done · 1.0s

Hypothesis: The FOMC × fwd-1h directional edge from

calendar_events(+50 bps, t=2.28, n=52) survives robustness checks: bootstrap 95% CI excludes zero, win rate ≥ 60%, effect present in both pre-2024 and post-2024 sub-samples, and removing the single most extreme observation still leaves > 30 bps.Verdict: LIKELY EDGE — REQUIRES MONITORING — 3/4 gates pass. Failing: bootstrap CI low > 10 bps. The +50 bps mean is plausible but with notable fragility. Acceptable for live testing as a small position-size strategy; not a 'high conviction' allocation.

Key metrics

| metric | value |

|---|---|

| n_events | 52 |

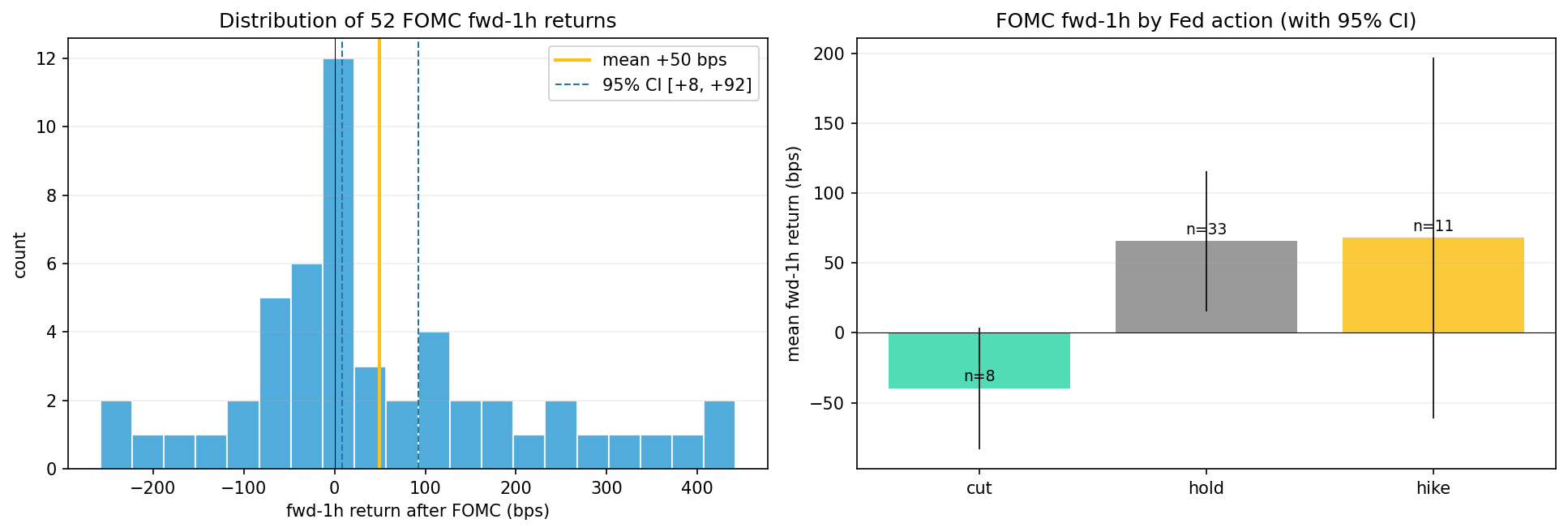

| mean_fwd_1h_bps | +49.8816 |

| ci_low_bps | +8.0730 |

| ci_high_bps | +92.3073 |

| win_rate_fwd_1h_pct | +57.6923 |

| trimmed_mean_bps | +48.1973 |

| early_half_mean_bps | 112.57 |

| late_half_mean_bps | +16.6912 |

| by_action_cut_bps | -39.7520 |

| by_action_hike_bps | +67.9017 |

| by_action_hold_bps | +65.6042 |

| bps_change_slope | -0.0904 |

| gates_passed | 3 |

| gates_total | 4 |

Approach

Stress-test the calendar_events finding of +50 bps fwd-1h mean after FOMC statement release. 52 events covered (2020 - 2026). Each event annotated with its action (cut / hike / hold) and bps change. Robustness, sub-samples, outliers, Fed-action conditioning, and a pre-drift surprise proxy.

1. Robustness — bootstrap CI, win rate, t-stat

| horizon | n | mean_bps | std_bps | se_bps | ci_low | ci_high | t_stat | win_rate | pct_above_30bps |

|---|---|---|---|---|---|---|---|---|---|

| fwd_1h | 52 | 49.9 | 156.4 | 21.69 | 8.1 | 92.3 | 2.3 | 0.58 | 0.38 |

| fwd_4h | 52 | 73.8 | 256 | 35.49 | 4 | 144.8 | 2.08 | 0.58 | 0.54 |

| fwd_24h | 52 | 37.1 | 469 | 65.05 | -87.2 | 168.6 | 0.57 | 0.46 | 0.44 |

2. Outlier sensitivity

- Mean (all 52 events): 49.9 bps

- Drop largest (event 2021-07-28, fwd_1h=+442 bps): 42.2 bps

- Drop smallest (event 2023-03-22, fwd_1h=-258 bps): 55.9 bps

- Drop both (50 events): 48.2 bps

- Median: 15.9 bps

3. Sub-sample stability

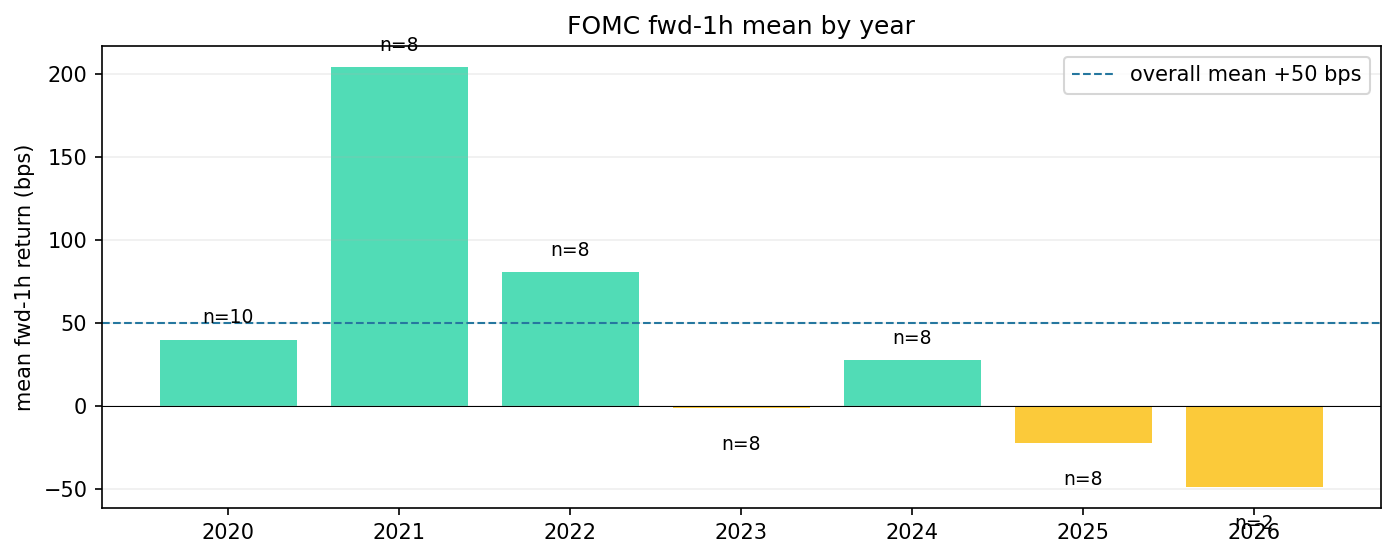

Per year

| year | mean | std | count |

|---|---|---|---|

| 2020 | 39.7 | 78.2 | 10 |

| 2021 | 203.7 | 172.5 | 8 |

| 2022 | 80.3 | 248.4 | 8 |

| 2023 | -1.6 | 125.6 | 8 |

| 2024 | 27.2 | 136.2 | 8 |

| 2025 | -22.6 | 84.1 | 8 |

| 2026 | -49.2 | 45.1 | 2 |

Halves

- Pre-2022 (n=18): mean 112.6 bps (win rate 78%)

- 2022+ (n=34): mean 16.7 bps (win rate 47%)

4. By Fed action (cut / hike / hold)

| action | n | mean_1h | std_1h | mean_4h | win_rate_1h | se_1h | t_1h |

|---|---|---|---|---|---|---|---|

| cut | 8 | -39.8 | 62.7 | 51.4 | 0.25 | 22.17 | -1.79 |

| hike | 11 | 67.9 | 218.6 | 63.9 | 0.55 | 65.92 | 1.03 |

| hold | 33 | 65.6 | 146.9 | 82.6 | 0.67 | 25.57 | 2.57 |

Rate-change magnitude effect (linear regression fwd_1h ~ bps change)

- slope: +1.355 bps fwd-1h per 1 bps Fed change (SE 0.702)

- intercept: +44.67 bps

- r: +0.263, p-value: 0.0594

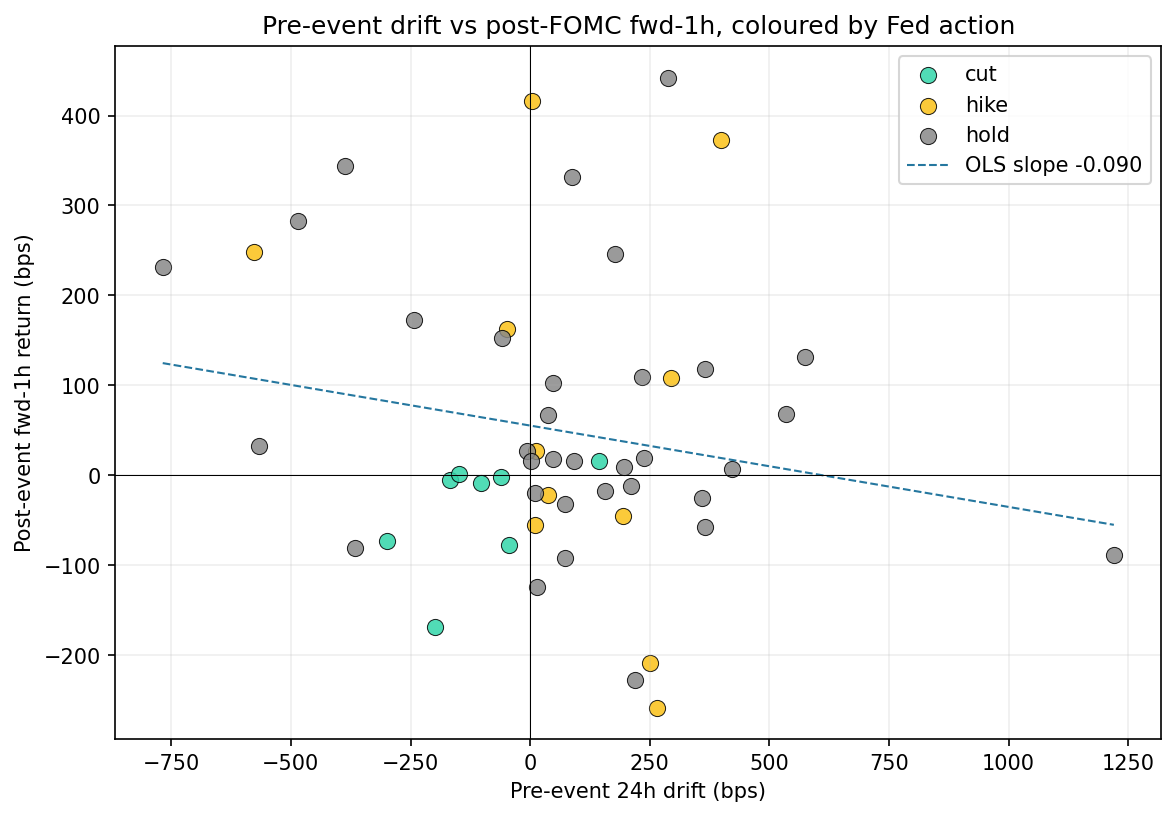

5. Surprise proxy — pre-event drift vs post-event return

Without external market-expectation data we proxy the 'consensus' by the BTC drift in the 24h leading into the meeting. Hypothesis: when BTC has already moved strongly in one direction before FOMC, the announcement either confirms (continuation) or surprises (reversal).

By pre-drift quartile (24h leading into FOMC)

| pre_q | n | pre_mean | fwd_1h_mean | fwd_1h_win | fwd_4h_mean |

|---|---|---|---|---|---|

| Q1 (down) | 13 | -336.4 | 74.9 | 0.54 | 141.8 |

| Q2 | 13 | 1.4 | 45.2 | 0.62 | 55 |

| Q3 | 13 | 146.4 | 31.1 | 0.54 | 16.6 |

| Q4 (up) | 13 | 428.7 | 48.3 | 0.62 | 82 |

Action × pre-drift sign

| n | fwd_1h_mean | fwd_1h_win | |

|---|---|---|---|

| ('cut', 'pre+') | 1 | 16 | 1 |

| ('cut', 'pre-') | 7 | -47.7 | 0.14 |

| ('hike', 'pre+') | 9 | 37.3 | 0.44 |

| ('hike', 'pre-') | 2 | 205.7 | 1 |

| ('hold', 'pre+') | 25 | 40.1 | 0.6 |

| ('hold', 'pre-') | 8 | 145.2 | 0.88 |

Production gates

| gate | pass? | actual |

|---|---|---|

| bootstrap CI low > 10 bps | FAIL | +8.1 bps |

| win rate ≥ 55% | OK | 57.7% |

| both halves positive | OK | early +113 / late +17 |

| trimmed mean > 25 bps | OK | +48.2 bps |

Passed: 3/4

Discussion — what the breakdown tells us

-

Cuts (n=8): fwd-1h -39.8 bps — no rally despite cut

-

Hikes (n=11): fwd-1h +67.9 bps — counterintuitive (hawkish should = risk-off)

-

Holds (n=33): fwd-1h +65.6 bps — usually the largest sub-group; if positive, the 'FOMC drift' is mostly here